Somewhere in my closet there’s a black BCW box with a strip of masking tape on the lid that just says “DON’T.” Inside it is most of the money I’ve spent on this game since college: a Revised dual land set I assembled one trade at a time, a couple of cards I’m too sentimental to sell, and a foil I genuinely could not replace if I tried. For years I never once thought about what happens to that box if a pipe bursts over it.

Then a friend’s basement flooded last winter, his Commander shelf got soaked, and I started thinking about it constantly.

So here’s the question I’ve been chewing on: should you insure your MTG collection? The annoying answer is that it depends on a number most people have never actually sat down and calculated.

Your homeowners policy almost certainly doesn’t cover your cards

The assumption most of us walk around with is that renters or homeowners insurance has us covered. House burns down, insurance pays, you rebuild, and the cards were “personal property” so they’re in there somewhere. That’s mostly not how it works for trading cards.

Standard U.S. homeowners, renters, and condo policies tend to treat collectibles as a special category, and trading cards usually land in the bucket that’s either flat-out excluded or covered up to a tiny sublimit. A lot of policies cap “collectibles” or similar valuables at something like $1,000 to $1,500 per claim. And even when they do pay, personal property often gets settled at actual cash value, which is to say depreciated value rather than the cost of rebuying the card at today’s market price. For a thing that appreciates, like a Revised dual, depreciated value is almost insulting.

The default state of your binder, then, unless you’ve gone and done something about it, is barely insured or not insured at all.

When a binder becomes an asset

The line people in the collectibles insurance world throw around is roughly $5,000. Below that, a dedicated policy usually isn’t worth the cost and hassle, and you’re better off just storing things well and accepting some risk. Above it, you’re effectively carrying an uninsured financial asset around in a cardboard box, and that’s worth a conversation with an agent.

The trouble is that most people have no clue which side of that line they’re on. They have a vibe, a number they say out loud at the LGS that’s probably wrong in both directions. If you’ve never actually priced your collection honestly, this is the part where it stops being academic.

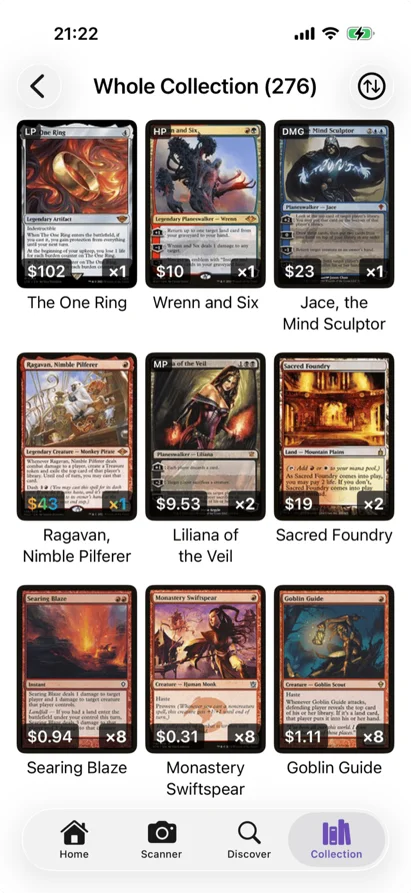

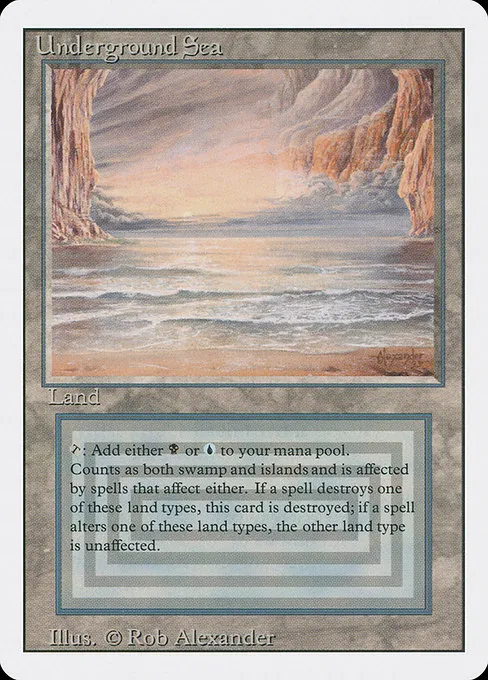

A single Revised Underground Sea runs around $930 right now. Add a playset of fetchlands, a few Commander staples that got expensive while you weren’t paying attention, an old Sheoldred you cracked and forgot about, and suddenly a “casual” collection is worth more than the laptop you’d insure without a second thought.

Honestly, I went back and forth writing this. Part of me thinks buying insurance on cardboard is a little ridiculous, and that the energy is better spent just not keeping your duals in a damp basement in the first place. For a lot of collections that’s genuinely the right call. But “store it well and hope” stops being a plan the moment the replacement cost crosses into four or five figures, and most growing collections cross that line without the owner ever noticing the day it happened.

Three ways to actually insure an MTG collection

If you decide your collection’s worth covering, there are basically three routes, and they aren’t equally good.

The first is a scheduled personal property endorsement, sometimes called a personal articles floater, bolted onto your existing homeowners or renters policy. You list items, assign each a value, and they get covered at replacement cost, usually with no deductible and on an open-perils basis (meaning it covers more than just fire and theft). Your insurer will want appraisals or proof of value. This is the cleanest option if your agent will write it for trading cards, which not all of them will.

The second is blanket coverage, where instead of listing each card you insure the whole collection under one raised limit. Less paperwork, no per-card appraisal, but usually a deductible and more fine print about what’s actually covered.

The third, and the one a lot of serious collectors land on, is a standalone collectibles policy from a specialty insurer. These companies (Collect Insure is the one that comes up most in MTG circles) write policies specifically for this. The numbers are more reasonable than you’d guess: I’ve seen a $35,000 collection insured for around $250 a year. Some of these are written as inland marine policies, which is the boring detail that actually matters, because it means your cards stay covered while they’re away from home, at the shop, at a tournament, in transit. If you play with your expensive cards, that’s the coverage you want.

For the record, I’m not an insurance agent, the rules vary by state and by company, and I genuinely don’t know how your specific insurer treats cards. Treat all of this as questions to bring to an agent and then verify, not gospel.

The documentation is the whole game

Every one of these options runs into the same wall: you have to prove what you had and what it was worth. After a fire or a theft, “trust me, there was a Mana Drain in there” is not a claim.

What insurers want is documentation that already exists before the loss. An itemized list with values. Photos. Ideally something timestamped so it’s obviously not assembled the week after your stuff vanished. For the standalone policies you don’t necessarily have to log every common; the guidance I’ve seen is to document something like 80% of the collection’s value, which in practice means the expensive pieces, the ones that’d actually move a payout.

And look. Nobody wants to do this. I know. Photographing and pricing your entire collection sounds like a weekend you’re never getting back. It’s the exact reason half of you have never priced your collection at all. So yeah. Documentation. Everyone agrees it matters, and nobody does it until something goes missing.

This is the one spot where the scanning apps earn their keep. Running a collection into something like Eldwyn spits out exactly the artifact an insurer asks for: a dated, itemized inventory with a per-card market value attached, exportable, sitting in the cloud instead of in the box that just got rained on. I scanned a long-box of my better stuff in an evening, and the side effect was learning the total ran a few hundred dollars higher than I’d assumed, which is its own quiet argument for doing it at all.

A couple of practical notes if you actually go down this road.

Graded cards are far easier to insure and value, because the slab and the grade give an objective reference an adjuster can’t argue with. If you’ve already sent cards off to PSA or BGS, you’re halfway to documentation already.

Insurers also care how you store things. “Fireproof safe, climate-controlled” gets you a better conversation, and a possibly better rate, than “shoebox under the bed.” Conveniently it’s the same stuff that keeps your cards in good shape regardless.

And update the thing. Prices move, you keep buying, and the collection you scanned two years ago looks nothing like the one in your closet now. An inventory that’s three years stale is most of the way to useless, which is also why insurers tell you to re-appraise annually.

I still haven’t actually called my insurance company, for whatever that’s worth. The box still says DON’T. But I did finally scan it, so at least now I know exactly what I’d be crying about.